2011 was a year of ups and downs in the development of the semiconductor lighting industry. The good development momentum at the end of 2010 did not continue as expected in the industry. Under the multiple pressures of massive release of domestic production capacity, slowing down of global market demand, and unclear government subsidy policy, China's semiconductor lighting industry began to enter the industry restructuring. And the new phase of the transformation of the competitive model. On the whole, despite the fact that many companies did not have satisfactory business conditions in 2011, and some companies even closed down, it is undeniable that the semiconductor lighting industry in China is still being further consolidated and is still the fastest growing region in the world.

Judging from the actual development situation throughout the year, although the international macroeconomic situation continues to fluctuate and the domestic industry investment form is still severe, the application scale and industry level of China's semiconductor lighting industry has still been significantly improved, and all sectors of the industry have remained relatively With a high growth rate, great progress has been made in the operation of domestic capital. Seven companies have achieved IPO and seven companies have had meetings. LED projects continue to be hot spots for capital chase. At the same time, in some areas where the investment in the previous stage was too concentrated, the industry competition became fierce, and SMEs that did not have advantages in terms of technology, cost, scale, and capital faced severe competition pressure.

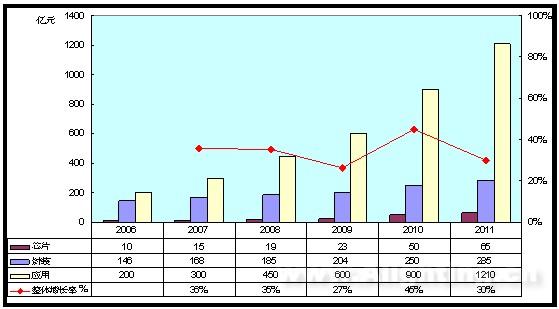

In 2011, the scale of China's semiconductor lighting industry reached 156 billion yuan, an increase of 30% from 120 billion yuan in 2010. The scale of upstream epitaxial chips, midstream packaging, and downstream applications was 6.5 billion yuan, 28.5 billion yuan, and 121 billion yuan respectively, with a slight slowdown in growth.

China's semiconductor lighting industry in 2011

Since 2009, the company's investment in MOCVD has been reflected in 2011. In 2011, in the second half of the year, many companies postponed the installation of equipment. With the addition of 320 new MOCVD units in China, the total number of MOCVD in China reached 720, and the production capacity of epitaxial wafers increased rapidly. According to the equipment introduction plan adjusted by each company, it is expected that the installed capacity of MOCVD will be maintained at around 300 units in the next year.

In 2011, domestic enterprise chip revenue increased by 30% to 6.5 billion yuan, but it was far below the 106% growth rate of MOCVD equipment. This also reflects that domestic chip production capacity has not been fully realized and the price pressure of epitaxial chips will continue to be sustained. In 2011, the domestic GaN chip production capacity increased to 12,000 kk/month, but the capacity utilization was less than 50%. The annual output was only 71 billion, but the localization rate reached over 70%. At the same time, domestic chips have achieved breakthroughs in lighting applications through the integration of small chips, but the market share of high-power lighting chips is still low, less than 20%.

In 2011, the scale of China's LED packaging industry reached 28.5 billion yuan, an increase of 14% from 25 billion yuan in 2010, and the output increased from 133 million in 2010 to 182 billion, an increase of 36%. Among them, the output value of the high-brightness LED reached 26.5 billion yuan, accounting for more than 90% of the total LED sales. From the point of view of product and enterprise structure, the growth of SMD LED packaging is the most obvious, and has become the mainstream product of LED packaging, and the proportion has been greatly improved.

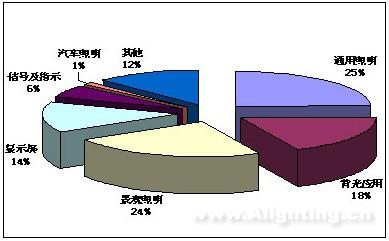

In 2011, the overall scale of China's semiconductor lighting applications reached 121 billion yuan, and the overall growth rate reached 34%, which is the fastest growing link in the semiconductor lighting industry chain. Among them, the growth of lighting applications is very obvious, the overall share has accounted for 25% of the entire application, becoming the largest market share of applications, backlight, landscape and other applications also maintained a rapid growth. It is expected that lighting applications in the domestic LED lighting will continue to be the fastest growing application area in the next few years and will become the key element in driving the entire semiconductor lighting industry in China. According to statistics from the pilot cities of “Ten Cities and Ten Thousand Peopleâ€, currently there are more than 2,000 demonstrative projects implemented in 37 pilot cities, with over 4.2 million LED lamps and more than 400 million kWh of electricity.

Distribution of Semiconductor Lighting Applications in China in 2011

From the perspective of the overall development of the industry, the development of the semiconductor lighting industry in China in 2011 presented the following outstanding features:

1, LED lighting market penetration rate is still low indoor lighting market started

China's lighting applications have accelerated significantly, and its application effects have been gradually recognized, but its penetration rate in the lighting market is still low. The domestic LED lighting application market has not yet become the dominant force in the development of the industry, forming a situation of “with space and no marketâ€. At present, the domestic semiconductor lighting industry, especially the downstream application industry, is still too dependent on the international market.

Domestic lighting application hotspots are moving from outdoor lighting to indoor, especially in commercial, industrial, and subway applications, and the demonstration effects of numerous application projects have been recognized. Although the industry's unanimously expected LED product subsidy policy has not yet been introduced, indoor lighting applications are still in its infancy, but its market application prospects have been recognized.

2. Industrial investment gradually returns to rationality, capital changes, industrial structure becomes stronger

Driven by the investment policies of local governments in previous years, the number of upstream outbound equipment increased rapidly in 2011. However, due to technical, talent, and market demand constraints, the production capacity is not satisfactory, and product performance has not achieved a substantial breakthrough. Technology and talent are still The biggest obstacle to upstream epitaxial chips. In the case of poor overall industry conditions, the blindness and repetitive investment momentum in various regions have been curbed, and rational consideration of industrial development has made industrial investment more cautious. For example, in the first half of the year, as the sapphire substrate project started to fall, the production release price rapidly fell to 10 US dollars in the second half of the year, and companies stopped building or abandoned their investment, and began to rationally think about the direction of investment.

The influence of capital on the development of the industry has gradually deepened. Industry competition is not only a competition of technology, products and markets, capital will change the industrial structure to a great extent. Expanding financing channels through public offerings and transactions in the securities market, and occupying an active position in the increasingly fierce competition in the industry, has become the pursuit of many companies for further development.

3. International giants accelerate the deployment of domestic industry consolidation

The potential size of China's LED lighting market has attracted the attention of international LED companies, and the process of lighting application has also brought more and more significant impact on the development of the entire semiconductor lighting industry. Because of the dual purposes of exploiting the domestic market and utilizing domestic manufacturing advantages, international companies are stepping up the pace of domestic industrial deployment and bringing changes to the domestic industrial competition landscape.

The turbulent international industrial environment and intensified competition in the industry have increased the pressure on corporate investment and profitability. Domestic semiconductor lighting has begun to accelerate its differentiation and industrial integration has begun to emerge. Enterprises with capital, scale, technology, brand, and market channels have become the main players in industrial integration, and the distribution pattern of domestic semiconductor lighting companies is gradually improving.

4. The government fully deploys the industrial innovation environment to further improve

2011 was the first year of China's "12th Five-Year Plan" period, and it was also a year for the Chinese government to fully deploy the semiconductor lighting industry. The Ministry of Science and Technology further strengthened the support for semiconductor lighting technology innovation, and approved the second batch of pilot cities for pilot cities of “Ten Cities, Ten Thousand Citiesâ€, and will further develop qualified supplier catalogs and recommended product catalogs. The National Development and Reform Commission clearly proposed the establishment of a leader system, and jointly issued the "Announcement on Gradually Prohibiting the Import and Sale of Incandescent Lighting Incandescent Lamps" by the Ministry of Commerce and the AQSIQ. The Ministry of Finance’s policy on subsidy for semiconductor lighting products is also coming soon.

At present, technology, patents, and standards are still the main constraints for the development of China's semiconductor lighting industry, especially in 2011, when the development of the industry enters the adjustment stage. In 2011, China made new explorations in the technological innovation model and the construction of public R&D platforms. It relied on the Semiconductor Lighting Alliance, initiated by five domestic and foreign research institutes, and participated in the establishment of the National Key Laboratory of Semiconductor Lighting Joint Innovation by 22 companies. Successfully started, through focusing on industrial common key technologies and leading-edge technology research, following the principle of joint, open, and sustainable, building an open, international semiconductor lighting public technology research and development platform with first-rate equipment, first-rate mechanism, and first-rate talents. In order to become China's semiconductor lighting industry to seize the commanding heights of industrial development strong support. The National Standards Committee has established the leading group and expert group for semiconductor lighting standards jointly with the National Development and Reform Commission, the Ministry of Science and Technology, the Ministry of Industry and Information Technology, the Ministry of Finance, and the Ministry of Housing and Urban-Rural Development to make overall planning, overall coordination, and comprehensively promote the development of the standards system. The industrial development environment has been further improved.

It is expected that in 2012, with the launch of the “Twelfth Five-Year Plan†work, the introduction of relevant supporting policies, the promotion of the scale of lighting applications, and the stability of the international economy, the development of the semiconductor lighting industry in China will improve in the second half of the year. SMEs' operating and financial pressures will not be significantly reduced, and leading companies in all sectors of the industry will have the opportunity to use their scale, technology, capital, market and brand advantages to expand their leading position through industry consolidation. Domestic semiconductor lighting industry A dominant brand system will also gradually form and the overall industry landscape will change accordingly. In 2012, China's semiconductor-based lighting industry will not significantly change the pattern of the industry, but the introduction of relevant domestic policies will further enhance the importance of the domestic market. The actual performance of semiconductor lighting listed companies will greatly affect the direction and scale of industrial investment, and the speed of industrial integration will further accelerate. Leading international companies will also gradually realize the domestic industrial layout, which will also make the domestic industry competition more complex.

For domestic semiconductor lighting companies, shaping their core competencies and brand image to form a clear product and technology line will be the most critical issue in the industry competition in 2012 and beyond.

New Energy Harness,Electronic Harness Customization,Pvc Electronic Harness,Automotive Electronic Harness

Shenzhen huaxunde Technology CO.,Ltd. , https://www.huaxundekj.com