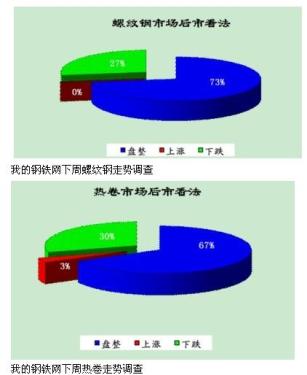

According to a survey of 46 steel mills and 133 traders in 15 cities in Shanghai including Shanghai, Tianjin, Guangzhou and Xi'an, the “My Steel Network†shows that the market is stable and bearish next week.

According to a survey of 46 steel mills and 133 traders in 15 cities in Shanghai including Shanghai, Tianjin, Guangzhou and Xi'an, the “My Steel Network†shows that the market is stable and bearish next week. In all the survey samples, circulation providers and steel mills were bearish for the next week's threading market at 27%, consolidating at 73%, and rising at 0%; for the HRC market next week, it was bearish at 30%, consolidating at 67%, rising to 3%. As the next week began to gradually leave the market for the Spring Festival holiday, the market has begun to close, and the terminal, whether it is site or steel mills, will not have too many purchases. The large percentage of shocks seen this week also shows that the market is now close to the “stopping the market†for the Spring Festival.

According to the trend of my steel net next week's hot roll investigation, the market still continues the trend of weak downward trend, among which the long-term decline is more obvious, and the flat steel is stable. As of Thursday, the Myspic Composite Index closed at 153.2 points, down 0.70% on a week-to-week basis. The long products index closed at 174.9 points, a week-on-month decrease of 1.06%. Flat products closed at 134.4 points, down 0.27% on a week-to-week basis.

This week, at the domestic macro level, the Bureau of Statistics issued a series of data such as CPI and PPI on Thursday. The data showed that the CPI in December rose by 4.1% year-on-year to a 15-month low. In December, PPI rose 1.7% year-on-year, a record low for two years. With the steady fall of inflation and the slowdown in domestic manufacturing demand, some analysts believe that the current inflation issue is not the main regulatory target, and may later be converted to “guaranteed growthâ€. After the release of data in December, the expectation of the RRR cut for the year before began again. However, we have seen from the deposit and loan data for December, and the Central Bank’s suspension of the central bank bill operation and the implementation of reverse repurchase on time. It is likely that management will not be eager to introduce monetary policies such as RRRs under the effect of year-end holiday prices.

On the foreign front, the U.S. economy’s recent steady economic recovery trend is evident. Its manufacturing ISM index has remained at an expansion range of more than 50% for 29 consecutive months, and the consumer and employment indices have also been significantly improved. Affected by this, European and American capital markets still perform well this week. . Of course, we cannot ignore the impact of the European crisis here. Due to the deterioration of employment and consumption in the EU countries, especially the rumors recently that the French rating may be lowered in the next few days. Prior to this, Italy and Spain were also rated agencies. Give "warning."

The iron and steel industry itself, due to the Spring Festival in January is the traditional off-season consumption, the market activity is extremely low, from the situation we understand, most traders have started a holiday next week, there are few to stick with the deal, after all It is still early for the factory and site to leave on holiday. Affected by this, the steel price continued to fluctuate this week. Among them, cold rolled steel, wire rods, and heavy plates all hit new lows during the year. In terms of production, the data from the China Steel Association on Monday showed that the average daily output of crude steel in the country in late December was 1,66.4 thousand tons, which represented a decrease of -2.38% from the previous period, which was the lowest output recorded during the year. From the recent ex-factory prices of Baosteel, Anshan Iron and Steel and Wuhan Iron and Steel in the last three months, basically flat and individual small preferential policies were opened. In the steel market, demand is low, cost pressures are still heavy, and corporate earnings are low. Under the constraints, a modest reduction in production may be a "wise" choice.

Although the overall output of steel is gradually falling down the channel, due to the unfavorable prices and transactions, domestic steel stocks show greater pressure. According to my steel network statistics, as of January 6, the country’s accumulated steel inventory was 13.343 million tons, a month-on-month increase of 413,200 tons, an increase of 3.2%. The stock of rebars was 5,171,600 tons, a month-on-month increase of 312,300 tons, an increase of 6.43%; wire stocks were 12,110,000 tons, a month-on-month increase of 239,300 tons, an increase of 24.63%; hot-rolled stocks were 4,404,800 tons, a month-on-month decrease of 14,190,000 Ton, a decline of 3.39%; cold-rolled stocks 1.5076 million tons, an increase of 0.44 million tons month-on-month, an increase of 0.29%. As a whole, the decline in sheet stocks is better than long products. The decline in plate inventory was mainly due to a slight recovery in the manufacturing industry's economy and a slight recovery in demand. This was confirmed by the fact that the PMI index rose by 1.3 percentage points from the previous month back to the boom line in December, but its sustainability is still difficult to guarantee at present. ; Long products stocks do not fall, but it is affected by the seasonal off-season consumption.

On the demand side, we have discussed many times before in the past changes in demand including railways, roads, automobiles, and home appliances, as well as the seasonal demand that is currently constrained by weather and holidays. This week we turned to external demand. On the 10th, the customs import and export data showed that domestic exports continued to slow down in December. Although exports in early November had improved due to the influence of external Christmas and European Christmas shopping season, the overall decline in external demand in the latter period may also Continuing, even though the U.S. economy began to show marked recovery, the trade friction between the U.S. and China has become even more pronounced under the weak global economy. In the emerging markets with better performance in the early stages, from December's data, Brazil, India, and South Korea all experienced a sharp drop from last month. Like the problems facing China, the weak external demand has been transmitted to more emerging market countries. The supporting role of emerging market demand for Chinese exports has continued to weaken.

Next week, no matter if it is a construction site or a manufacturing plant, or if we are struggling to make a round of a year in the steel market, we will continue to go home on holiday. Farther home, they couldn't stop queuing for tickets all night long; people who were tired couldn't cover the joy of the whole family reunion. In comparison, the disinterestedness of the steel market in the next week is predictable. Under such circumstances, the transaction is almost stagnant. Looking at the large proportion of this week's sample of shock consolidation, it is already true to tell people that the New Year has arrived and the rest will save energy for the coming year!

Corn Sheller,Hand Corn Sheller,Corn Sheller Machine,Hand Crank Corn Sheller

Hunan Furui Mechanical and Electrical Equipment Manufacturing Co., Ltd. , https://www.thresher.nl